You can read the full report in PDF format here.

Bitcoin is the largest pool of pristine collateral in the world. Yet borrowing against it remains expensive, fragmented, and shallow. The result is a high-quality asset running on low-quality credit rails.

What's missing are expressive onchain loan markets and standardized, financeable claims. In mature systems, loans do not stop at origination. They trade, they get financed, and capital recycles. That recycling compresses rates and deepens liquidity. BTC-backed loans today largely end at origination.

A new generation of onchain architecture, exemplified by Morpho V2, opens the door to fixed-maturity, market-priced BTC loan claims that can be traded and financed.

For platforms building BTC-backed credit products, wallets, custodians, exchanges, and lending providers, this changes the underlying economics. When loan claims are standardized and financeable, funding costs fall. When capital can turn over instead of remaining trapped, longer maturities become viable. The result is more competitive products and stronger unit economics, without introducing new custody trade-offs.

This series explains the structure, the implications, and the limits.

Authors:

David Seroy, Head of Ecosystem, Alpen Labs

Kirk Hutchison, New Chains Growth, Morpho

BTC backed lending exists. We can originate loans, but we do not widely reuse claims, finance them, or scale them the way mature credit markets do.

DeFi evolved from orderbooks (ETHLend) to pools (Compound/Aave) to pools with isolated risk (Morpho V1). Liquidity scaled, but market structure was sacrificed: negotiated pricing and fixed-term credit were replaced by algorithmic, floating-rate pools.

ETHLend first attempted orderbook based lending but failed to attract liquidity. Morpho V2 restores orderbooks without sacrificing liquidity, enabling fixed-maturity, market-priced loans with passive capital.

Once loan claims are fixed-term and reusable, they can be traded, financed, and used to recycle capital. Onchain tokenization makes this transparent, low-friction and low-cost by default.

The cheapest credit flows to the lowest-trust systems. By minimizing custody, oracle, and governance discretion, onchain BTC credit can reduce counterparty risk and compress embedded risk premia.

Distribution has always required a custody tradeoff. Account abstraction breaks it. Onchain BTC-backed credit can now run inside products that feel nothing like crypto.

Standardized BTC-backed loan claims can function as reusable collateral inside onchain credit markets, similar to repo. Credit converges on the deepest, lowest trust, most reusable, most neutral collateral. Bitcoin has the size. This architecture builds the rest.

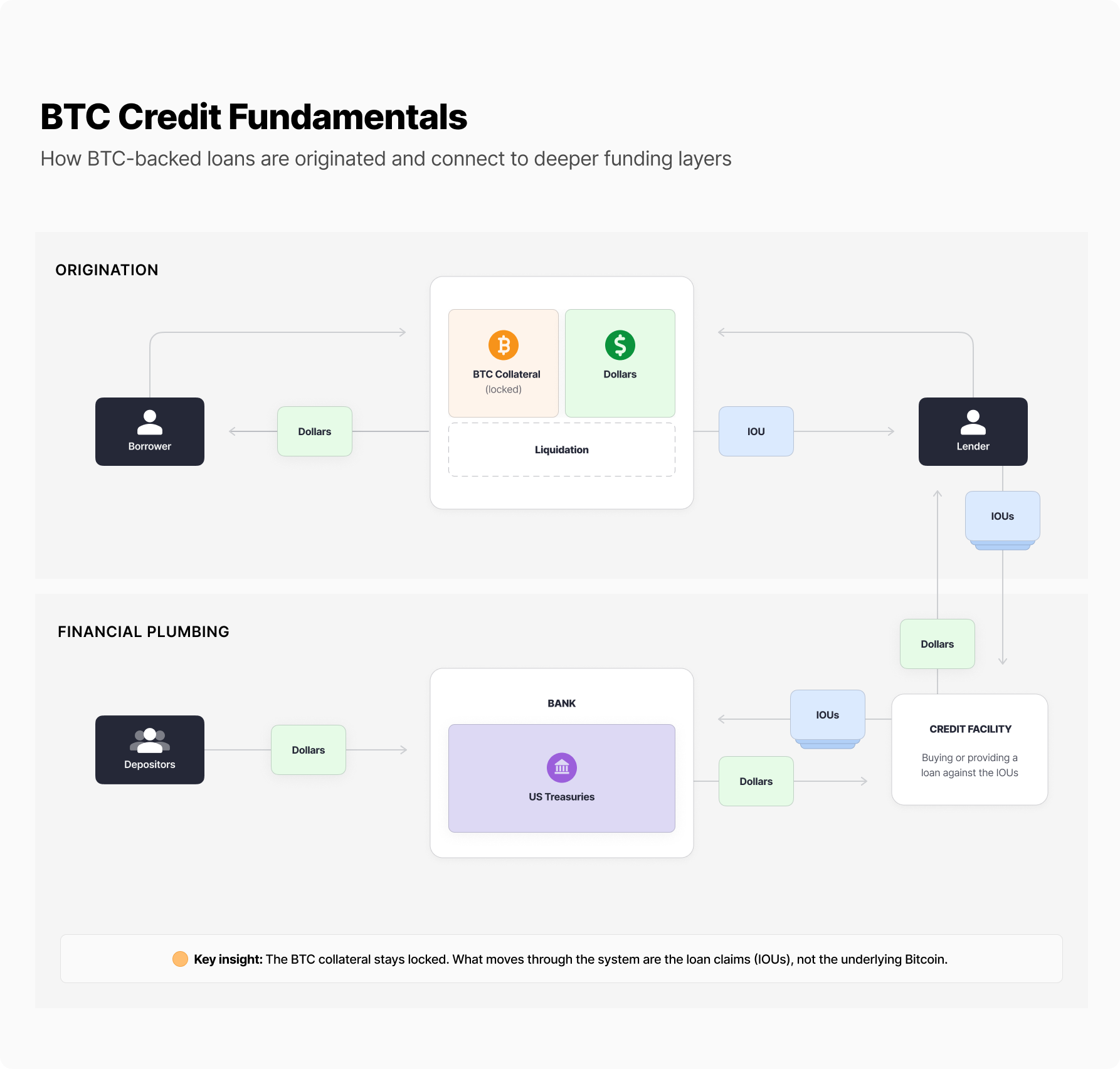

Borrowing dollars against BTC is no longer new. While products differ on the surface, every BTC-backed loan boils down to the same three questions: how BTC collateral is held, what happens if the loan goes bad, and where the dollars come from.

BTC custody generally falls into three buckets, each with different trust assumptions. Fully custodial models have a third party directly hold the BTC. Wrapped BTC locks coins with a custodian or bridge and represents them on another chain. Non-custodial designs keep BTC locked on bitcoin and enforce withdrawals through cryptographic rules rather than trusted intermediaries.

When prices move, liquidation infrastructure determines how BTC collateral is handled when a loan becomes undercollateralized. Clear, automated liquidation rules reduce uncertainty for lenders, which directly translates into lower rates, higher loan-to-value ratios, and more flexible terms for borrowers.

Dollar supply sets the hard limits on the system. Most BTC lenders rely on finite balance sheets or narrow funding channels, which constrains how cheap and how large these markets can grow.

These primitives are sufficient to originate BTC-backed loans. They are not sufficient to produce a credit market.

As demand for BTC-backed borrowing grows, available capital at borrower-friendly terms quickly runs out. Once that happens, borrowing becomes more expensive, less flexible, or unavailable altogether.

Mature credit systems solve this by extending beyond origination. Loans do not remain static. Once made, they become assets for the lender. Those assets can be sold, pledged, or combined to access additional financial plumbing. This allows capital to be reused and credit to continue expanding without relying solely on the original lender’s balance sheet.

This post-origination activity is less visible than borrowing itself, but it is what allows liquidity to circulate, costs to compress, and credit markets to scale.

Importantly, this does not require reusing the borrower’s collateral (rehypothecation). In a BTC-native system, the BTC itself can remain locked and verifiably segregated. What moves through the system are the loan claims held by lenders, not the BTC posted by borrowers.

The key takeaway from this chapter is that BTC-backed lending exists today, but BTC-backed credit markets do not, at least not at scale.

This framing raises the questions explored in the rest of the series. How can onchain architectures improve the primitives of BTC-backed lending? Can BTC-backed credit scale into deeper financial plumbing layers without inheriting the fragility of legacy systems? And if that architecture works end-to-end, how far could BTC-backed credit extend within global markets?

The next chapter looks at how early onchain designs approached these questions, and the structural reasons they fell short.

In the previous chapter, we separated BTC-backed loan origination from the broader machinery that allows credit to scale. With that framing, we can now examine how early onchain systems attempted to rebuild credit markets and why those designs plateaued.

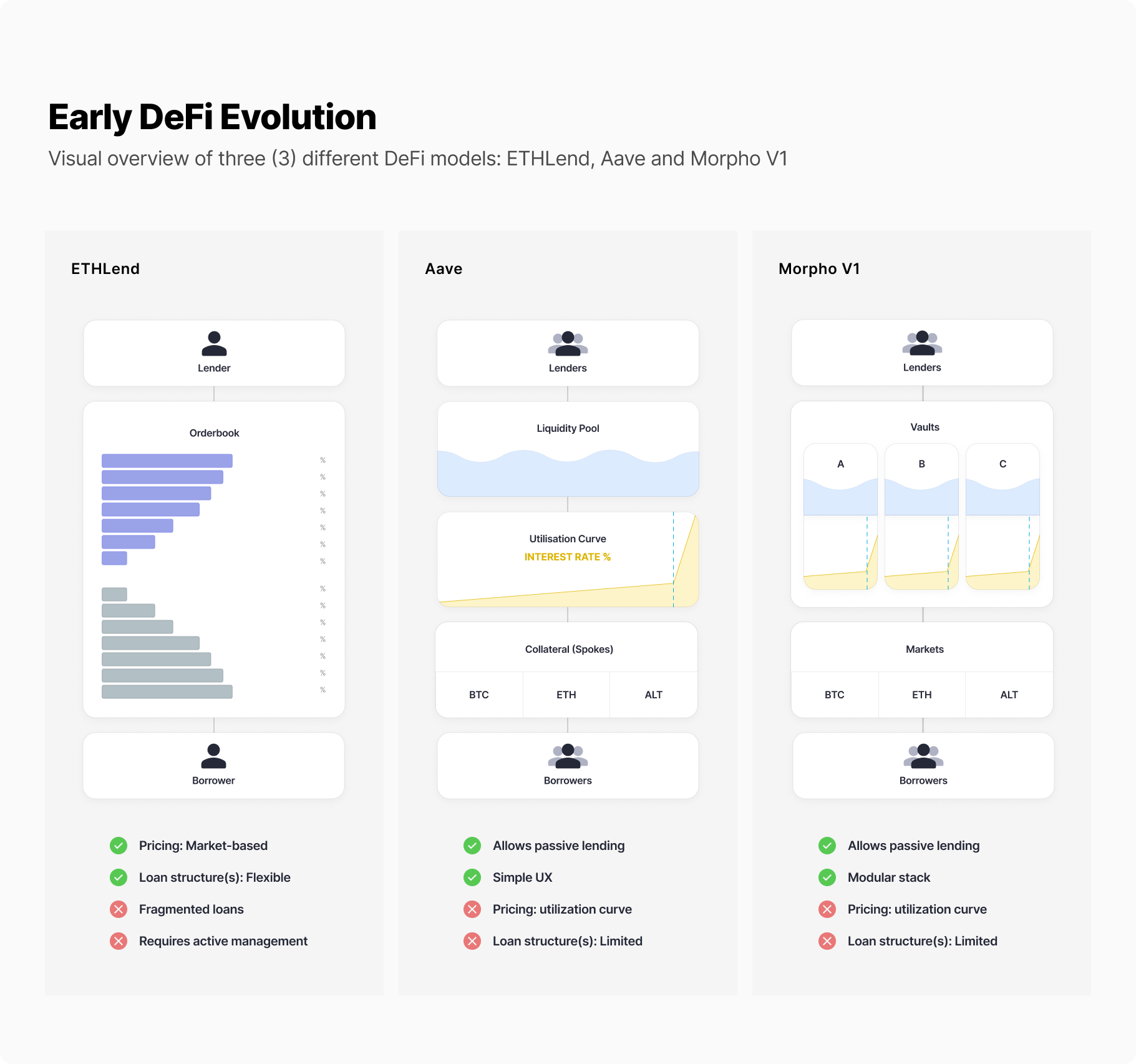

The first serious attempt at onchain lending was ETHLend. It used a direct peer-to-peer model: lenders posted offers, borrowers posted requests, and loans executed when terms matched. In theory, this is how markets should optimally work.

In practice, ETHLend failed to scale.

Every loan was bespoke. Liquidity scattered across thousands of small offers. Matching was slow and unreliable. Most importantly, the system assumed lenders would actively price and manage risk themselves. That assumption proved unrealistic. Without sophisticated market participants constantly updating quotes, markets stalled or drifted into stale pricing.

ETHLend was abandoned and pivoted to what we today know as Aave; the pool-based model was born.

The next design shift replaced orderbooks with pools. Protocols like Compound, and later Aave, aggregated liquidity into shared pools and set prices algorithmically using utilization curves. Lenders deposited capital passively, and borrowers drew from the pool.

In simple terms, the interest rate rises as more of the pool’s funds are borrowed and falls when liquidity is abundant. Price is determined by overall supply and demand for the pool, not by individual negotiation.

This worked.

Pooled lending removed the need for active participation. Liquidity bootstrapped quickly. Anyone could deposit capital and earn yield without managing pricing or risk. This “set-it-and-forget-it” model enabled permissionless capital formation at scale.

Over time, pooled systems improved. Newer designs, including Aave V4, introduced better risk segmentation, more granular configurations, and hub-and-spoke architectures to isolate assets and parameters. These changes materially improved safety and capital efficiency.

But the core structure remained the same.

Everyone borrows and lends based on the same utilization curve, and loan terms are standardized. Rates and terms do not emerge from negotiation; they are computed and set by an algorithm.

Pools solved ETHLend’s bootstrapping problem by flattening markets into a single configuration. They scale liquidity well, but they do not produce markets with flexibility.

Over time, the limitations became clear. Utilization curves are effective at aggregating liquidity, but they cannot express fixed terms, negotiated pricing, or heterogeneous risk preferences. Supporting those features requires creating new pools, fragmenting liquidity, or introducing active management, undoing the very simplicity that made pools scale.

These are not implementation flaws. They are structural tradeoffs.

DeFi thus far has succeeded by prioritizing liquidity over market formation. It created large lending systems, but not true credit markets.

Breaking past this ceiling requires an architecture that preserves the liquidity advantages of pools while reintroducing real market dynamics.

That problem, and how it is finally addressed, is the focus of the next chapter.

In the previous chapter, we saw why early onchain lending stalled. ETHLend tried to build markets with orderbooks but failed to attract liquidity. Pool-based systems like Aave solved that by making lending passive and scalable, but at the cost of uniform pricing and rigid loan terms.

Morpho V1 introduced an intermediate step: isolated risk.

Instead of a single global pool, Morpho enabled permissionless vaults, each running a distinct strategy. A curator defines the vault’s parameters, and any changes to those rules are proposed through a timelocked process. Lenders choose which vault strategy to allocate to.

This made risk opt-in and modular while preserving the liquidity advantages of pooled lending. But pricing remained algorithmic. Vault yields were inherited from the utilization curves of the underlying markets they allocated into. There was no negotiation of maturity, no fixed-term structure, and no true price discovery between counterparties.

A segmented pool can isolate risk. It cannot create term-structured markets.

Orderbooks reintroduce what pools with utilization curves cannot express: time, differentiated pricing, customizable liquidation rules and explicit matching between borrowers and lenders.

This chapter introduces the next step.

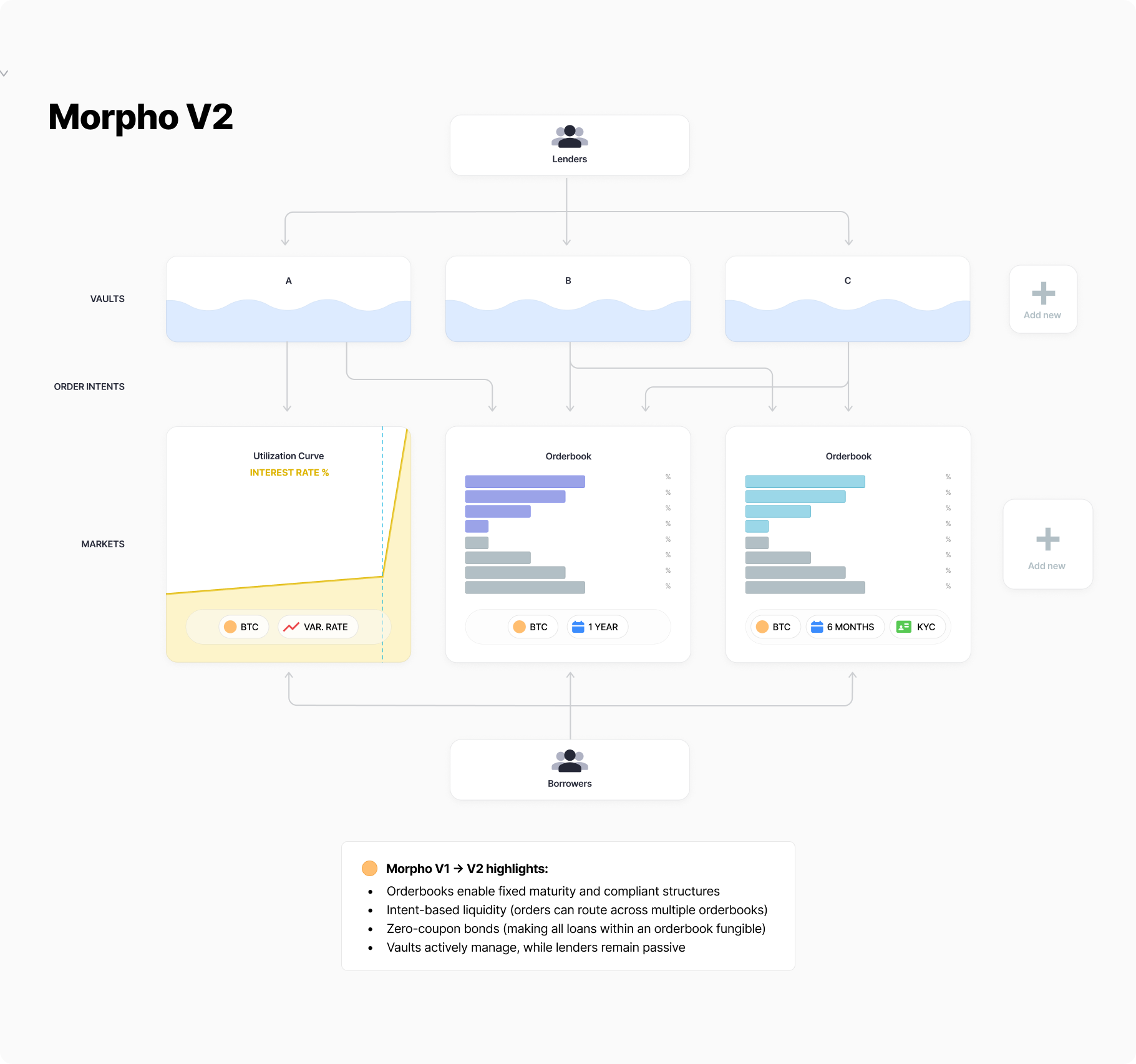

Morpho V2 does not abandon pools or utilization curves. It adds orderbooks alongside them, allowing markets to choose between algorithmic liquidity and negotiated term structure. To make orderbooks succeed, where ETHLend failed, three problems must be solved at once: performance, loan fragmentation, and active management. Morpho V2 addresses all three through four core innovations:

Together, these make real credit markets using orderbooks viable onchain.

Orderbooks require constant updates. Quotes change, offers are placed or canceled, and liquidity shifts as market conditions evolve. On a blockchain, every update costs gas. If every lender had to constantly post and refresh quotes onchain, markets would quickly become too expensive to operate.

Earlier attempts at onchain orderbooks struggled with this exact problem. Quoting was gas-intensive, and liquidity fragmented across inactive or stale offers.

Morpho V2 solves this without moving orderbooks offchain. Instead of forcing lenders to actively quote every price, V2 introduces intent-based liquidity.

Lenders do not continuously update orders. They specify parameters: collateral type, LTV, maturity, minimum yield and delegate execution. For example:

“Lend up to \$100M against BTC, 30–180 day maturities, at yields above 5%.”

That intent can be matched onchain when a borrower meets the criteria. The lender does not need to actively manage individual quotes or pay gas for constant updates.

This approach keeps the orderbook onchain while dramatically reducing the gas cost of participation.

Liquidity becomes programmable rather than manually quoted.

Capital is no longer locked into a single pool or waiting for a perfect counterparty. It flows wherever matching conditions are met. Quotes are effectively abstracted into rules rather than individual transactions.

Early orderbook lending struggled because every loan was its own contract. Even if two loans shared the same collateral and maturity, different interest rates meant different agreements.

In effect, every loan became its own micro-market.

If a lender wanted to exit early, they had to find a buyer for that exact loan. Without a standardized unit, depth could not aggregate across positions. Each transfer required a bespoke negotiation, spreads stayed wide, and secondary markets never meaningfully formed.

Morpho V2 solves this by representing loans in each orderbook as standardized zero-coupon obligation units. Suppose an orderbook is for BTC collateral at 150% collateralization (67% LTV), maturing December 31, 2026.

A lender provides \$10,000 at a price implying 10% APY. Instead of recording “10% interest,” the protocol mints 11,000 loan units. Each unit redeems for \$1 at maturity.

Another lender may provide \$10,000 later and receive 10,800 units, implying a lower yield. The rate is embedded in the price paid for units. Once minted, however, all units in that orderbook are identical claims: \$1 payable at the same maturity under the same collateral terms.

Because the units are fungible, any lender can sell some or all of their position at the prevailing market price. The orderbook remains active until maturity, allowing continuous trading of exposure rather than one-time loan transfers.

Instead of bespoke loans that must be held to expiration, lenders hold standardized units. Fungibility concentrates liquidity. Concentrated liquidity tightens spreads and enables continuous price discovery.

By standardizing repayment into identical units, Morpho V2 transforms isolated bilateral contracts into a true term-structured market.

Orderbooks still require active management. Prices must be updated, exposure controlled, and risk managed in real time. Expecting retail lenders to do this is unrealistic.

In Aave, all lenders deposit into large shared pools with one global configuration per market. Morpho V1 changed this by introducing vaults, which act like smaller, configurable pools. Each vault is managed by a curator who defines the risk rules, while lenders simply deposit and remain hands-off.

In Morpho V2, the role of curators as risk managers extends naturally to orderbooks. Curators now also take on active market management, pricing and adjusting offers on behalf of passive lenders. What was originally designed to give risk optionality maps cleanly onto the need for sophisticated, continuous active management in orderbook markets.

Curators cleanly bridge the gap between the desire for permissionless, passive liquidity formation from retail LP and the active management required for efficient price discovery in orderbooks.

This architecture doesn’t just improve pricing. It changes what kinds of loans can exist onchain.

With orderbook-based, fixed-term markets, loans can be defined around specific terms: maturity, collateral type, oracle choice, liquidation rules, and participation constraints. Instead of one pool with one rule set, you can create distinct markets for distinct requirements.

For example, an institutional market could require verified counterparties, longer maturities, use a specific price feed, and route liquidations through a permissioned liquidator that can offer grace periods or margin-call style workflows. Another market may require variable rates, specific oracles and higher LTV. The key is that these markets can be bespoke without losing liquidity, because intents and curators keep capital flexible and passive.

Because vaults can allocate across multiple differentiated markets, their shares represent exposure to curated portfolios of BTC-backed loans.

Vaults begin to resemble structured BTC-backed credit portfolios. Competition between curators naturally drives optimization around vaults to create the best risk-adjusted portfolios. In later chapters we’ll explore how these begin to function like bitcoin-collateralized loan obligations (“bCLO”).

Taken together, this architecture supports market-driven pricing, flexible loan terms, and scalable liquidity without forcing users to become sophisticated market makers.

What it does not yet address is what happens after loans are originated, how positions move, are financed, and connect to deeper funding layers. That post-origination layer is where credit truly scales.

The next chapter turns to that layer: loan standardization, secondary markets, and financial plumbing.

So far, this series has focused on how BTC-backed loans are originated and priced onchain. What we have not yet examined is what happens after a loan is made.

For borrowers, credit often ends at origination. Collateral is posted, dollars are received, and the interaction stops. For lenders, origination is only the beginning.

In mature credit markets, loans do not remain static. Once originated, a loan becomes a financial asset owned by the lender. That asset can be reused rather than simply held until repayment.

This reuse is what allows credit to scale without relying solely on fresh capital. Two closely related mechanisms make this possible: loan standardization and secondary markets.

Loan standardization turns loans into reusable assets. Similar loans are grouped and represented by standardized claims with defined cash flows and risk characteristics.

Secondary markets allow those claims to be easily bought, sold, or financed.

Importantly, neither of these directly affect the borrower. Loan terms remain unchanged and collateral stays locked (not rehypothecated). What changes is how lenders manage and reuse their assets behind the scenes.

Together, these mechanisms let lenders sell packages of loans, borrow against them, and redeploy the proceeds as they see fit.

Historically, DeFi lending has been dominated by pool-based models (like Aave and Morpho V1). Pools deliberately flatten all loans into the same homogenized structure: floating-rate, no maturity, instant redemption. There is no discrete underlying loan to sell, no subset to bundle, and no differentiated cash flow to finance.

That simplicity removes the need for loan standardization or secondary markets. It also places a ceiling on how flexible credit markets can be.

Morpho V2 breaks the pool abstraction and restores differentiated loan structures.

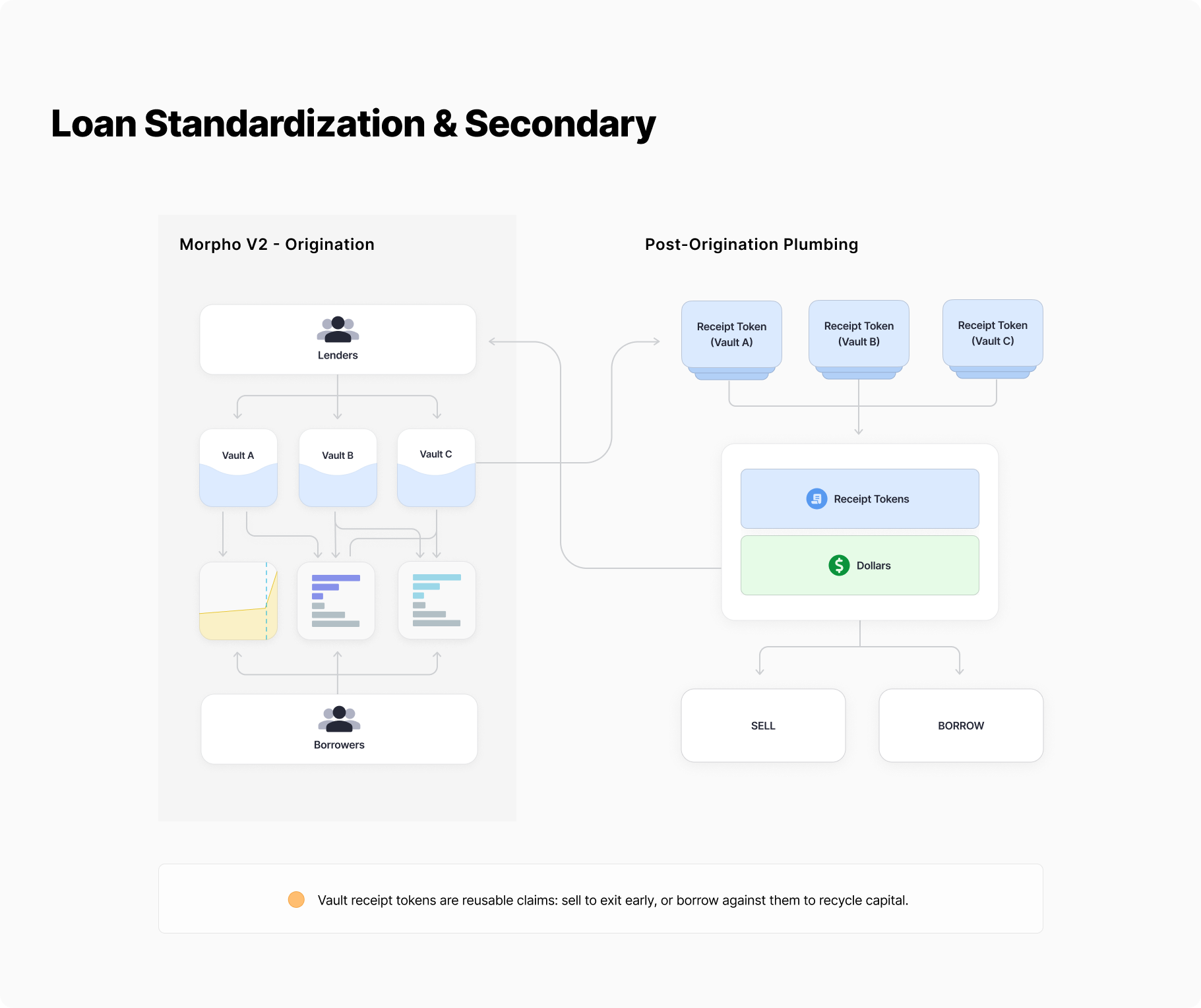

Vaults can hold short-duration floating loans, longer fixed-maturity loans, or a mix of both. Because loans are no longer identical, redemption and liquidity depend on portfolio structure rather than a single global pool.

Vaults issue Vault Receipt Tokens (“receipt tokens”) as standardized, yield-bearing, dollar-denominated claims backed by overcollateralized BTC-secured loan portfolios. Lenders hold these tokens instead of generic pool shares.

Because receipt tokens are native onchain assets, the infrastructure to reuse them already exists. They can be sold on DEXes, pledged as collateral in lending markets, or incorporated into carry strategies.

At that point, receipt tokens stop behaving like simple accounting shares and begin functioning as collateral objects that are transparent, overcollateralized, verifiable, and programmatically enforced.

That composability changes the economics. A lender can sell a longer-duration receipt token to exit early. Another lender can use it as collateral to borrow short-term at a lower variable rate while continuing to earn the vault’s higher fixed yield, capturing the spread. When capital can exit or be financed, fixed-term rates no longer need to carry a large lockup premium. Over time, longer-dated borrowing costs compress toward short-term variable funding rates.

Offchain, achieving this requires legal structuring and trusted intermediaries. Onchain, it emerges directly from standardized, tokenized claims governed by transparent smart contracts.

Secondary markets for receipt tokens did not fail to form in DeFi because the tooling was absent. They failed because pooled lending reduced all loans to interchangeable, floating-rate shares, eliminating the discrete claims needed for financing and resale.

Morpho V2 changes that. By introducing differentiated, fixed-term loan claims, it makes financing and resale economically meaningful without affecting borrowers or their collateral.

When loan claims can be financed or exited early, balance sheet arbitrage emerges. Capital can loop, capture spreads, and compete away excess term premia. As spreads compress, borrowing costs fall and longer maturities become viable.

With that foundation, BTC-backed credit can scale the way mature credit markets do: by recycling capital, repricing risk, and connecting origination to deeper liquidity.

As credit markets grow, participants become increasingly sensitive to counterparty risk, governance structure, and operational assumptions. These factors may be tolerable at small scale but become material as credit deepens.

This chapter maps where trust lives in the BTC-backed credit stack, how far it can be reduced through design, and where it remains unavoidable.

At the base of this architecture sits Morpho itself. Morpho is designed as immutable, low-level infrastructure. The rules governing settlement, vault accounting, and permissions are not meant to change arbitrarily.

Trust is not embedded in the base protocol. It is introduced by the components built on top of it.

In this architecture, trust concentrates in four places:

All of these are ultimately bound by governance and upgrade authority.

The collateral layer is the hardest constraint in BTC-backed credit.

Most BTC-backed lending relies on wrapped BTC. For example, WBTC locks BTC with BitGo and issues an asset on Ethereum, while cbBTC locks BTC with Coinbase and issues an asset on Base. This is simple for users but places control of the BTC with a custodian.

From a credit perspective, this introduces counterparty risk at the collateral layer. If policies change, withdrawals are restricted, or custody is compromised, the collateral backing the credit market is affected regardless of how well the lending protocol itself is designed. It also undermines neutrality. When a BTC asset is controlled by a single custodian, it becomes harder for competing platforms to adopt it, limiting its usefulness as a shared credit primitive.

Recent advances make it possible to reduce this trust assumption. Using BitVM-style techniques and garbled-circuit verification, BTC-native designs such as Glock aim to reduce custody trust to a 1-of-N model. No single party can move funds unilaterally; a single honest participant is sufficient to prevent theft.

This does not eliminate trust entirely but materially reduces discretionary control at the collateral layer. Practically speaking, it represents the lowest-trust way to use BTC in onchain credit systems without requiring changes to bitcoin itself.

Vaults and curators define how lender capital is deployed, not who owns it.

A vault functions like a small lending fund. A curator sets its rules: what collateral is accepted, how strict liquidations are, which price feeds are used, and how much risk the vault can take. Lenders choose whether to deposit and, by doing so, explicitly opt into that curator’s risk profile.

Curators do not custody funds and cannot move user assets. Their authority is limited to configuration. But poor configuration can still increase risk. A curator might accept weak collateral, use unreliable oracles, or set loose liquidation thresholds.

That risk is opt-in and visible. Multiple vaults can coexist. Lenders are not forced into one global rule set. Markets can price curator quality directly.

Vault isolation limits damage to opted-in participants. It does not prevent bad curators from existing. What keeps curators honest over time is market discipline. Curators who perform poorly lose deposits to better alternatives. Those with skin in the game, whether through fee structures tied to performance or capital at risk alongside depositors, have stronger alignment. Lenders should treat curator incentive structures as part of their due diligence, not an afterthought.

Oracles determine prices and trigger liquidations. This is an unavoidable trust surface in any onchain credit system.

Oracle failures take different forms. A price feed might lag during extreme volatility, report stale data during an outage, or be manipulated through flash loan attacks.

Oracle risk can be reduced through decentralization, redundancy, and conservative configuration, but it cannot be eliminated. Major oracle providers like Chainlink, Redstone, and Chaos Labs have secured billions in DeFi protocols and proven resilient through multiple market cycles and stress events. While battle-tested infrastructure reduces risk, the dependency itself remains unavoidable.

What matters for credit markets is that oracle assumptions are explicit. As with collateral and curators, the architecture allows choice. Different markets can rely on different oracle providers or configurations, allowing participants to select the level of trust and responsiveness they are comfortable with.

Liquidations are essential to credit markets, but design alone cannot guarantee smooth execution. When loans become undercollateralized, liquidators seize collateral and sell it on external markets to repay lenders. That assumes deep liquidity and reliable pricing. In calm markets, this holds. In stressed markets, it may not.

During sharp drawdowns, DEX liquidity often thins precisely when liquidations trigger. Slippage widens, pricing destabilizes, and liquidators may hesitate to take positions they cannot unwind. At that point, system safety depends less on code and more on market depth.

Execution venue also matters. Immutable venues like Uniswap minimize governance risk at the settlement layer. More expressive systems such as Fluid can offer richer routing and execution logic, but introduce additional upgrade and governance surface.

Many trust surfaces are additionally bounded by governance and upgrade authority.

While base protocol logic is designed to remain stable, bridges, vault parameters, oracle configurations, and some DEXes must retain upgrade paths. Without flexibility, a bug or oracle failure could permanently damage the system.

Well-designed governance limits authority. Permissions are narrow. Changes are transparent. Upgrades are slow, typically gated by timelocks that provide days or weeks for markets to react.

Governance cannot disappear, but it must be predictable. Slow and visible authority allows risk to be priced rather than blindly assumed.

Governance capture remains possible. A coordinated majority could push harmful upgrades after a timelock expires. The defense is distribution of power and the ability of markets to exit or migrate.

Onchain credit markets do not eliminate trust. They make it explicit and opt-in.

This architecture does not enforce a single trust model. Participants choose which BTC representation to use, which curator to trust, which oracle to rely on, which governance model to accept.

Over time, capital concentrates around the most reusable, neutral, and lowest-risk configurations. The system does not dictate that outcome. It allows markets to discover and price it.

At this point, the structure is clear and the trust assumptions are explicit. Whether it becomes consequential now depends on distribution, whether these credit rails can reach users without reintroducing custody tradeoffs.

The next chapter turns to that problem.

Up to this point, the series has focused on structure: how BTC-backed credit can be originated, priced, reused, and governed onchain. What remains is whether that structure can reach users at scale.

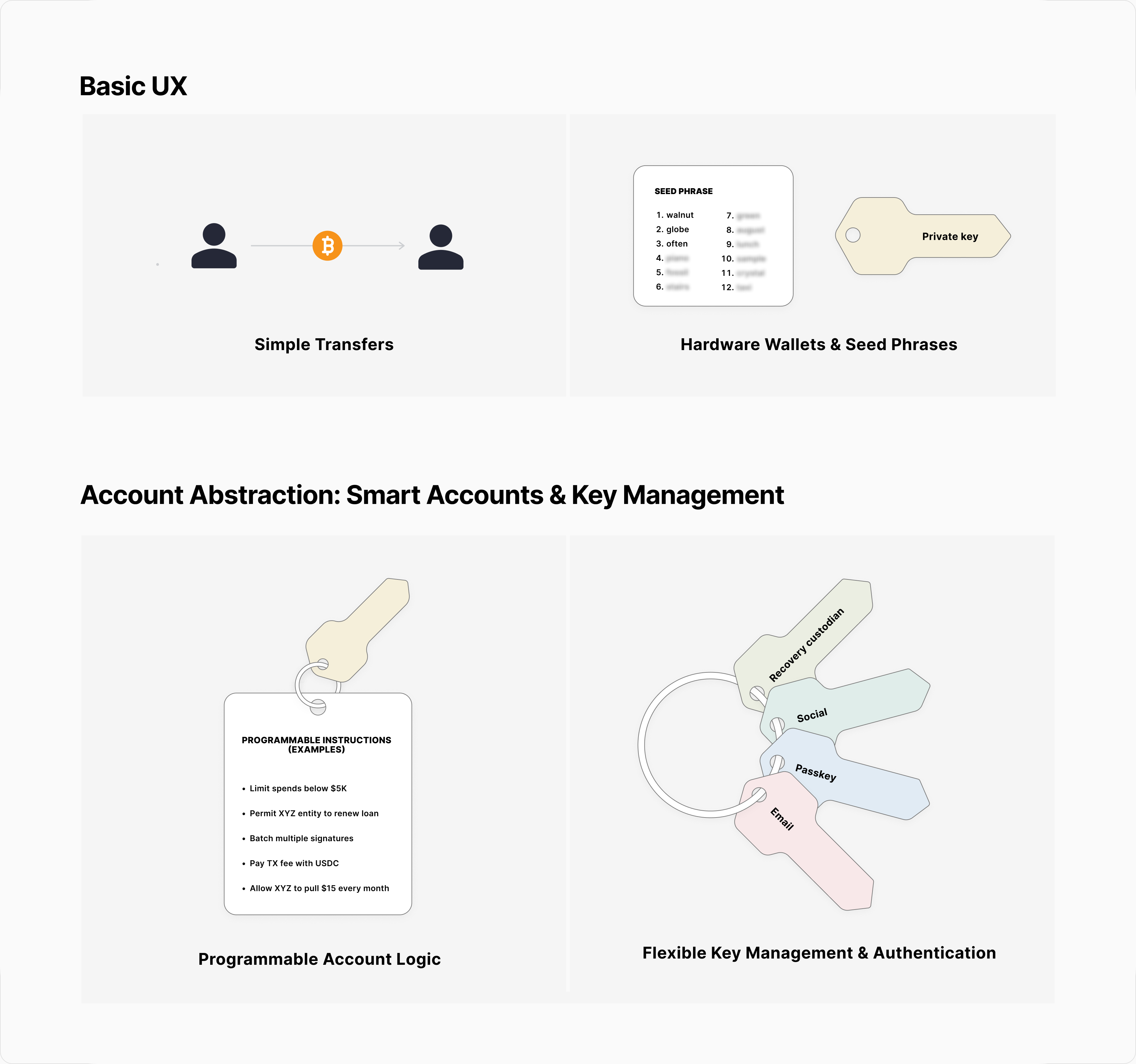

Historically, using onchain systems has been high-friction. Users must manage seed phrases, click through multiple approvals for a single action, and hold extra assets just to pay transaction fees. Much of this has nothing to do with credit itself.

At the same time, users want different things. Some want direct key control. Others want familiar interfaces and trusted distribution. A scalable credit system has to support both without forcing custody tradeoffs or a single UX model.

In practice, this breaks into two questions: who controls the account, and how the account behaves.

Key management determines how users authenticate and how keys are protected.

Modern key management services improve onboarding without forcing custody. Providers like Privy and Dynamic let users access non-custodial accounts using familiar authentication such as passkeys, biometrics, or email-based flows, while still retaining cryptographic ownership. More advanced setups can support distributed signing and institution-grade policies.

The point is optionality. Users and institutions can choose the key setup and operational complexity they’re comfortable with.

Traditional wallets behave like manual signing devices. Every step requires a separate transaction and signature.

Account abstraction changes that by making the account programmable. Instead of signing every individual step, users approve an intent and the account enforces rules around what is allowed.

Concretely, this unlocks:

Together, key management and account abstraction separate credit rails from user experience.

Distribution partners can keep the UX they want while running non-custodial credit under the hood. This is the “DeFi mullet”: fintech in the front, DeFi in the back.

The Coinbase–Morpho integration shows the shape. The user experience can feel familiar: passkey sign-in, fewer approvals, fees handled automatically. Underneath, the credit logic remains onchain and non-custodial.

This makes BTC-backed credit embeddable into existing products and workflows rather than requiring users to adopt new tools or mental models.

Account abstraction doesn’t force one experience. It expands the design space. Strict self-custody, guided experiences through trusted distributors, and everything in between can coexist on the same credit rails.

This removes painful UX from being a bottleneck to distribution.

The final chapter looks at where this architecture converges. If BTC-backed credit can scale markets, constrain trust, and distribute cleanly, how far can it realistically go?

Up to this point, this series has been about proving something practical: BTC-backed credit can be built onchain with market-driven pricing, reusable loan instruments, explicit trust boundaries, and distribution that does not force custody tradeoffs.

This final chapter asks a different question. If this architecture works, how far could it go?

Modern credit markets revolve around a simple principle: the largest pools of capital lend cheapest when loans are short-term and secured by collateral that is universally trusted.

That is the role repo plays in traditional finance. High-quality collateral is posted, dollars are borrowed, and if the borrower fails, the collateral is sold. Repo functions as a base funding layer because the collateral is liquid, standardized, and easy to finance.

US Treasuries sit at the center of this system. Not because they are perfect, but because they are the most financeable collateral available at scale. Their widespread acceptance allows them to be funded cheaply and reused continuously throughout the credit system. That structural demand is part of why sovereign borrowing costs remain low.

The system works, but it depends on access to “safe” collateral and the institutional structures that govern it.

Now bring that lens back to this architecture.

Morpho V2 vaults issue standardized receipt tokens representing dollar-denominated claims on future repayment from overcollateralized BTC-backed loans. These receipt tokens function as BTC-collateralized loan obligations, or bCLOs: enforceable by code, transparent onchain, and backed by segregated BTC.

bCLOs invite comparison to Treasuries. Both are debt instruments backed by an underlying balance sheet. Both are future claims on dollars plus interest. The difference is the counterparty. Treasuries rely on the full faith and credit of the US government. A bCLO relies on overcollateralized BTC with liquidation enforced programmatically.

Treasuries earn a structural premium because they are the most desired collateral in global funding markets. Demand for them lowers their funding cost and reinforces their dominance.

The question is whether a native onchain credit system converges on tokenized Treasuries or produces a structurally superior form of collateral.

Platforms like Aave already finance volatile assets such as WBTC and cbBTC at high loan-to-values often above 80 percent and low single-digit borrowing costs under normal conditions. That is with purely volatile collateral.

A bCLO upgrades that profile. It strips out directional BTC volatility while preserving BTC’s depth and neutrality. And unlike tokenized Treasuries, it does not rely on offchain custodians or freeze controls that introduce additional risk premia.

If markets are already willing to lend cheaply against wrapped BTC, a structured, dollar-denominated BTC claim with lower volatility and fewer custodial dependencies is a credible candidate for even better funding terms.

This changes incentives.

Some participants will hold bCLOs for yield. Others will hold them because they unlock the cheapest, highest-leverage access to credit in the system.

The motivation shifts from “I want BTC exposure” to “I want the most financeable collateral in the system.”

Winning the title of most pristine collateral carries a premium. For Treasuries, that privilege allows the US government to borrow at exceptionally low rates. In a BTC-native system, if bCLOs become preferred collateral, the premium does not accrue to a sovereign. It compresses borrowing costs for BTC-backed credit itself.

In that model, the benefit flows to savers rather than to the state.

If bCLOs become widely accepted collateral, a reinforcing loop emerges.

BTC-backed borrowing creates standardized claims. Those claims become preferred funding collateral. Liquidity concentrates around them. As liquidity deepens, funding costs compress and usable LTV rises. Better terms increase demand to originate and hold more bCLOs.

This is how collateral hierarchies form. Capital converges on the instrument that is easiest to finance at scale, and that demand lowers the cost of issuing it.

For this dynamic to hold, the earlier architecture must prove itself in practice.

Loan markets must support differentiated terms at scale without fragmenting liquidity (Chapter 3). Loan claims must be genuinely tradable and financeable in secondary markets (Chapter 4). Collateral custody and governance must remain credibly neutral and resistant to discretion (Chapter 5). Distribution must not reintroduce custody tradeoffs (Chapter 6).

If those constraints hold, the architecture stops being theoretical. It becomes structurally competitive as a native credit substrate.

The practical conclusion of this series is straightforward: onchain BTC credit can now be built with real market structure: differentiated lending markets, standardized loan claims, capital reuse, and bounded trust surfaces.

The ambitious conclusion is structural. If bCLOs become the most financeable, transparent, and neutral collateral inside onchain funding markets, liquidity will concentrate around them. As liquidity deepens, borrowing costs compress, issuance grows, and the system compounds.

History shows that credit expands until it meets its constraint. That constraint is collateral. When collateral cannot scale, systems manufacture substitutes, stretch for synthetic safety, and eventually fracture.

A durable release valve is real savings: collateral that can absorb scale without hidden leverage, rehypothecation, or discretionary control. Only verifiable, non-sovereign assets with deep monetary premium can play that role.

Bitcoin is the largest pool of pristine savings in the world. For the first time, it now has credit architecture capable of expressing that scale.

Size without architecture is wasted potential. Architecture without size is a toy. Bitcoin finally has both.

———

If this direction resonates and you’re exploring BTC credit, feel free to reach out to us at credit@alpenlabs.io.

© 2025 Alpen Labs. All rights reserved.

.svg)